- April 8, 2025

“A nickel ain’t worth a dime anymore.” – Yogi Berra

The famously quotable Yankee, whether intended or not at the time, aptly described the impact of inflation on the value of our money. In recent times when headline inflation has barely been above zero, it can be difficult to recall eras in our recent past when inflation was near the historical average of 3% much less the double digit years of the late 1970’s and early 1980’s. The fact remains that the long term erosion of the value of a dollar due to inflation has the potential to pose the greatest risk to future financial needs and goals. Whether the goal is to generate income during retirement years, accumulate funds to for tuition, or to leave a legacy, it’s important to consider the impact of inflation on those goals.

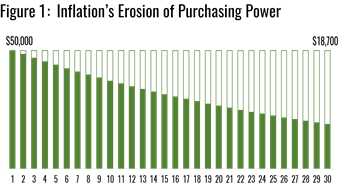

Suppose you begin retirement expecting to spend $50,000 per year to meet all of your goals. In your second year of retirement, that same $50,000 might only buy you about $48,000 worth of “stuff” due to inflation. This might not seem like a big difference, but when we expect to spend approximately 30 years in retirement, that initial $50,000 will only buy you approximately $19,000 worth of “stuff” at the end of 30 years if inflation averages 3% per year. Figure 1 shows the declining value of the initial $50,000 year by year.

A common belief is that as one approaches or enters retirement and begins withdrawing from their portfolio, a higher allocation of bonds is warranted to “preserve capital”. While bonds do, in fact, preserve capital, the capital they preserve does not grow over time with inflation and effectively becomes less valuable over time in real terms. To see this in action, suppose you were to attempt to meet the $50,000 spending goal by purchasing a high quality $1,000,000 bond that pays 5% interest. This strategy will ensure the delivery of $50,000 every year that can be spent plus returning your initial $1,000,000 investment upon the bond’s maturity in 30 years.

The static nature of these interest payments is why bonds are often called “fixed income” investments. The problem with this approach is that by the end of the 30 years, the $50,000 of interest has become the equivalent of $19,000 (Figure 1) and the $1,000,000 paid back from the bond is the equivalent getting paid back only $392,000 after adjusting for inflation. For this reason, the goal should be to preserve purchasing power rather than capital.

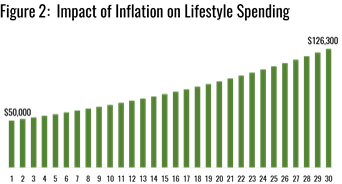

To help understand the need to preserve purchasing power, Figure 2 shows that $126,000 will need to be spent in 30 years to live the same lifestyle that cost $50,000 in the first year. A focus on preservation of capital and fixed income as a means of investing more conservatively or taking on less risk in attempt to ensure one’s financial security in retirement actually creates more risk to the success of one’s retirement lifestyle! Preserving purchasing power requires a shift in focus from fixed income to growth of income. Specifically, income that can be expected to grow at or above the pace of inflation.

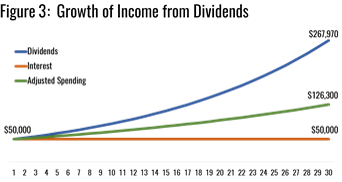

Luckily for all investors, there has been, and remains to be, an investment from which we can expect to achieve the required growth of income to preserve one’s purchasing power against the wrath of inflation. Figure 3 shows that while a fixed income interest payment of $50,000 remained the same for 30 years, $50,000 in dividend income grew to $267,000 per year over 30 years. This has been possible because dividends are paid out of corporate earnings, which have a centuries-long track record of inflation-beating growth that has allowed dividend growth to average approximately 6% per year on average or about double the rate of inflation. In this example, dividend income has also grown to exceed the $126,000 needed per year to sustain one’s lifestyle allowing for excess income to be reinvested for future goals.

At the time of this writing, the interest rate on a 10-year US Treasury bond (a common proxy for market yield) is 2.3% and the dividend yield on the S&P 500 stock index is 1.9%. Though the interest from the bond is slightly higher at the time of purchase, it will remain fixed over its life while dividends can be expected to grow in excess of inflation to protect and grow the purchasing power of those payments. It is true that stocks do fluctuate in price more than bonds, but, as we saw in last quarter’s letter, those fluctuations prove to be temporary. There is a place in a well diversified portfolio for both stocks and bonds, but an over reliance on bonds before and during retirement in an effort to be “more conservative” or to “preserve capital” can actually pose greater risk to one’s long-term financial security.

Thank you again for allowing us to serve you and please let us know if you have any questions or comments. We always look forward to hearing from you.

Best wishes,

The Partners of PrairieView