- July 8, 2025

In my last post, I included Warren Buffet’s quote that investing should be simple but it’s not always easy. Diversifying investments among several different categories of stocks with different economic, financial, and business circumstances seems to be quite simple, at least on the surface. Modern investment vehicles and technology have, in some respects, made investing simpler than ever. We’re effectively in a “golden age” for low-cost, tax-efficient investing. However, the proliferation of investment categories and products has, in other respects, made it more complex than ever. The paradox of choice, combined with a never ending flow of information, can make it difficult to construct an effectively diversified portfolio and stick to it.

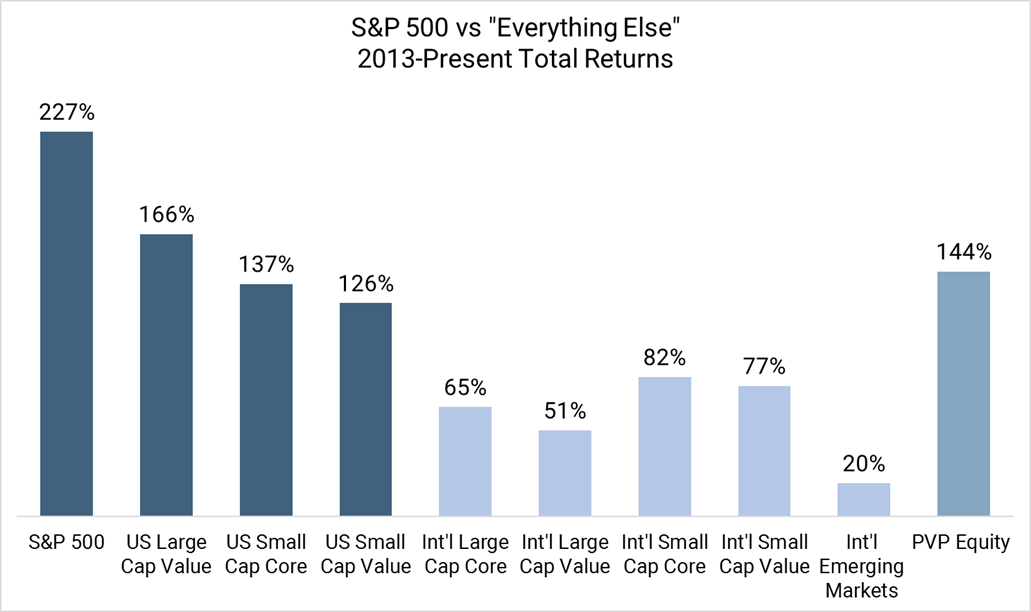

Over the last ten or so years, perhaps one of the hardest things has been to maintain a diversified portfolio when year after year, with few exceptions, the S&P 500 has beaten nearly every other stock category. It’s become easy to look back and think, “if only we’d have just invested in the S&P 500.” Or, to consider throwing diversification to the wind and join the “what’s been working lately” team, expecting that it will keep working.

Figure 1: Over the last 10 years, the Growth-oriented S&P 500 has outperformed nearly every other major stock market. "PVP Equity" represents a diversified portfolio of all categories shown.

These thoughts are understandable given what we’ve recently experienced but they’re also short-sighted for three reasons:

- We never know what investment is going to perform best or otherwise in the future. Just like we didn’t know 10 years ago that the S&P 500 would be the best performer 10 years hence, we don’t know what will be the best performer 10 years from now.

- Large scale market cycles, tend to be rather slow-moving, change direction when least expected, and aren’t accompanied by a clear signal to dump one category in favor of the other.

- As long-term, goal-focused investors, we invest for much longer than 1, 5, or 10 years and need to invest in a way that prepares us for multiple cycles and an unknown future.

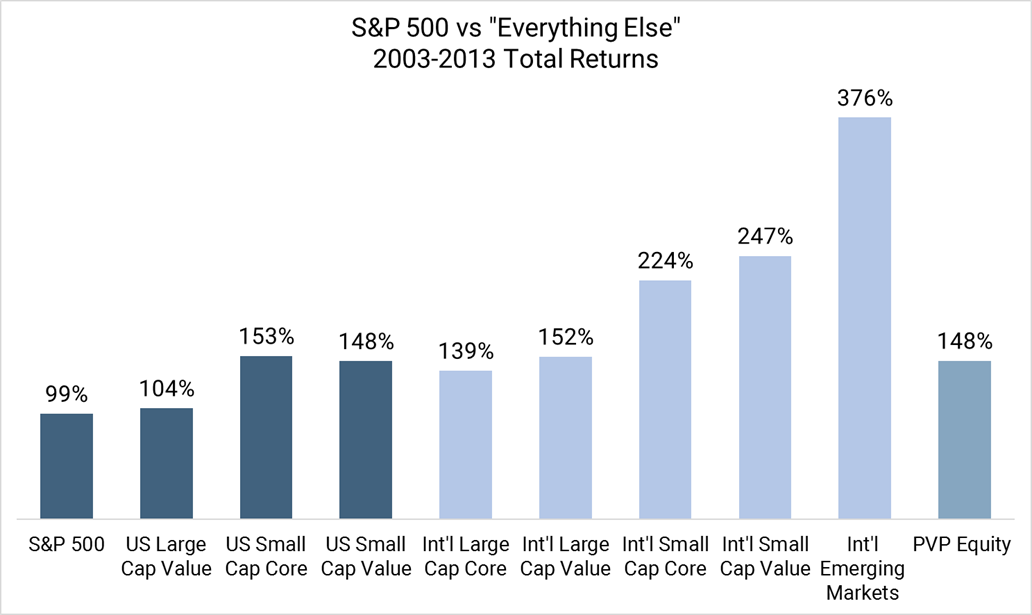

As evidence of the benefits of evaluating stock returns throughout multiple cycles, the 10 years that preceded the most recent 10 years provide an excellent example.

Figure 2: During the prior 10 years, the S&P 500 was the laggard among categories. Interestingly, the diversified "PVP Equity" had very similar performance in these two 10 year periods that saw very different performance among the individual categories.

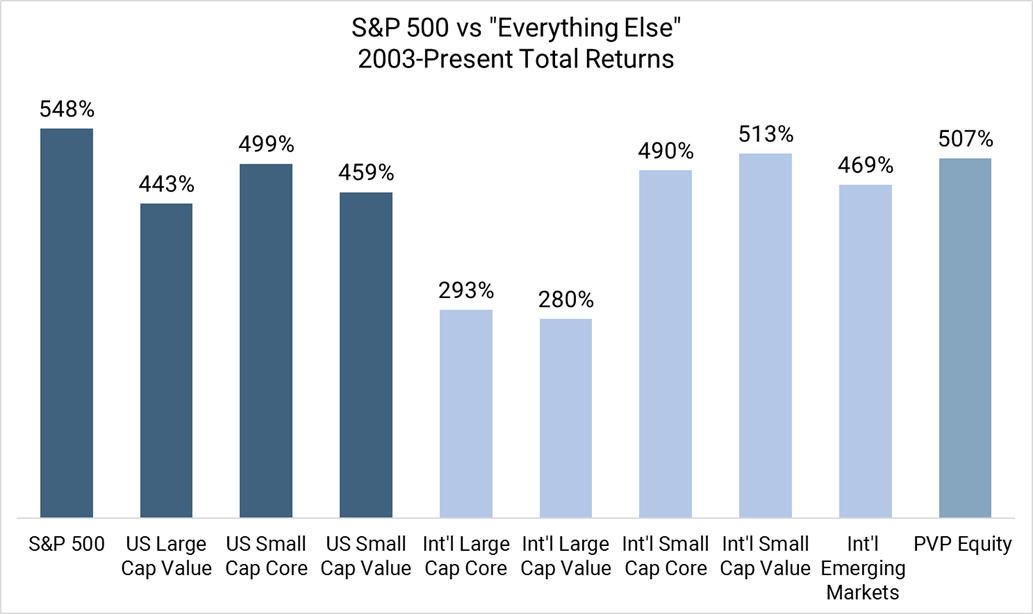

Figure 3: With only a couple exceptions, linking the two periods together shows similar performance among categories. Note: 20 year performance is not the sum of the two 10 year periods due to compounding.

The last 10 years’ relative outperformance of the S&P 500 and underperformance of Everything Else has left the S&P 500 with high expectations and high valuation. Everything Else has lower valuations that reflect lower expectations. The problem with high expectations is they become difficult to meet, but low expectations become easy to surpass. Market returns are driven by relative expectations rather than absolute results. It’s hard to know what stocks might be the best performers for the next 10 years, but we can consider a few historical examples and take stock of how the present compares.

The “Lost Decade”

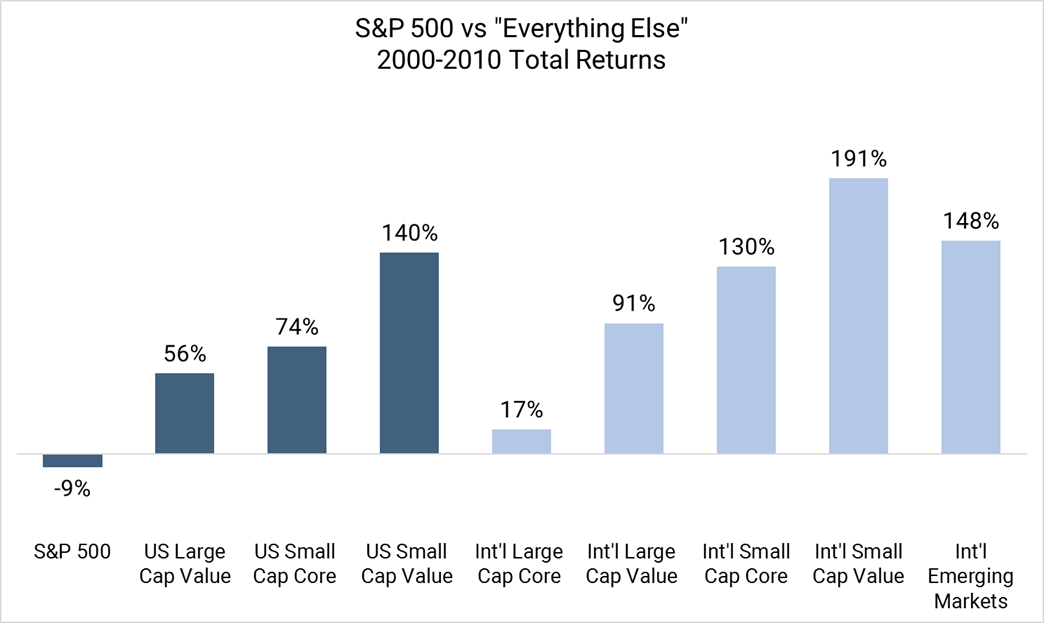

There was a widely held belief that the first decade of the 21st century was a “Lost Decade” for stock investors since the S&P 500 finished that decade with negative total returns. This is an understandable, if not somewhat obvious, surface-level conclusion as the decade began at the height of the dot com bubble and ended near the depth of the Great Financial Crisis. However, that couldn’t have been further from the truth for the diversified stock portfolio. During this time nearly all other major stock categories posted rather attractive returns. The “Lost Decade” for the S&P 500 was followed by its world beating returns that we have seen since.

Figure 4: The "Lost Decade" was only lost if one had only invested in the S&P 500.

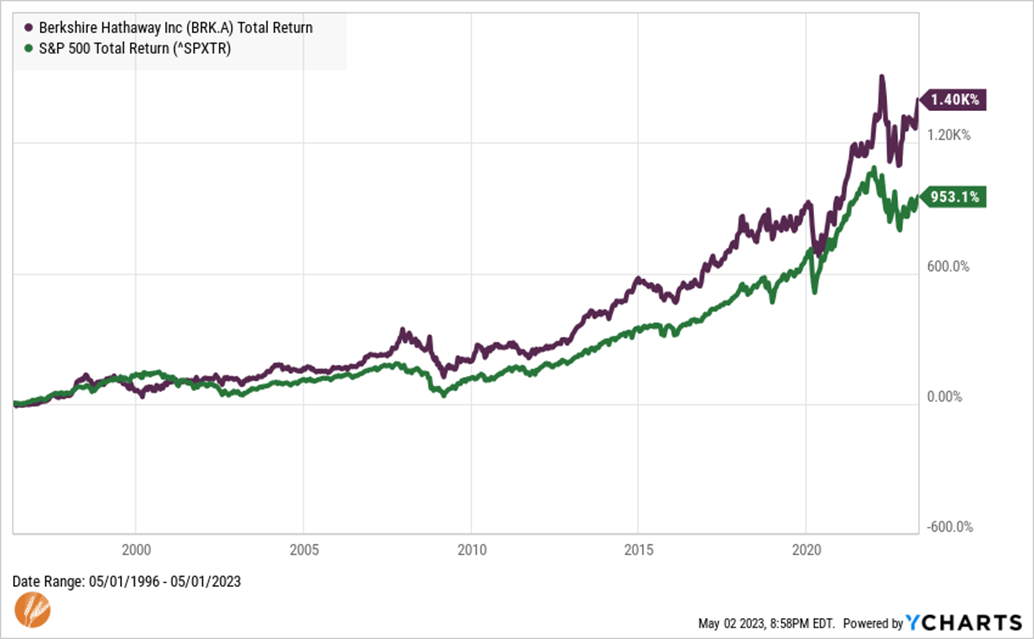

There was a time when Warren Buffet was said to have lost touch with “modern investing”

Prior to the “Lost Decade” was the boom in tech stocks, which was also a time when the S&P 500 and the tech-laden NASDAQ indexes outperformed nearly everything else. During this time Warren Buffet was said to have been out of touch with “modern investing,” having eschewed the high-flying tech stocks of the day in favor of his preferred low-price, value-oriented stocks of proven companies. The decline in tech stocks followed by attractive returns from low-price value stocks during the “lost decade” proved that he hadn’t lost touch with “modern investing.” Rather, he maintained discipline to remain invested in a strategy that has worked over longer time horizons.

Figure 5: Starting in the mid to late 1990's when Warren Buffet was said to have lost touch, the stock of Berkshire Hathaway has performed quite well through several market environments. This can be seen as evidence of the benefits of adherence to a proven strategy.

Emerging Markets during the S&P 500’s “Lost Decade”

Like low-priced value stocks during the tech stock boom of the 1990s, Emerging Markets stocks also struggled under the weight of a Russian debt default and a currency crisis with the Thai baht, among other challenges. This scenario may seem loosely similar to today’s environment. Emerging Markets’ struggles left them quite undervalued – even when compared to their bleak circumstances at the time. As the decade wore on, investors continued to reward Emerging Markets stocks for eclipsing increasing expectations. By the middle of the decade, the investing world was consumed with the future of Emerging Markets with the acronym BRICS, for Brazil, Russia, India, China, and South Korea, expected to dominate the future investment landscape. Eventually, the expectations and lofty valuations became a hurdle to future returns. This may sound similar to a more recent acronym of FAANMG, for Facebook, Apple, Amazon, Netflix, Microsoft, and Google.

The “Value Spread”

Research from the value-oriented investment manager AQR, and the employer of some the top researchers in quantitative finance, tracks what is referred to as the “Value Spread.” This is a basic measure of the difference in valuation between Growth (high-priced) stocks and Value (low-priced) stocks. It now indicates that Growth stocks, thanks in part to the aforementioned FAANMG companies, are the most overvalued relative to Value stocks since the height of the dot com boom of the late 1990s. This potentially bodes well for Value stocks’ future performance relative to the Growth-heavy S&P 500. Of course, things can always become more overvalued in the short-term.

US stocks are priced for perfection and International stocks are cheap

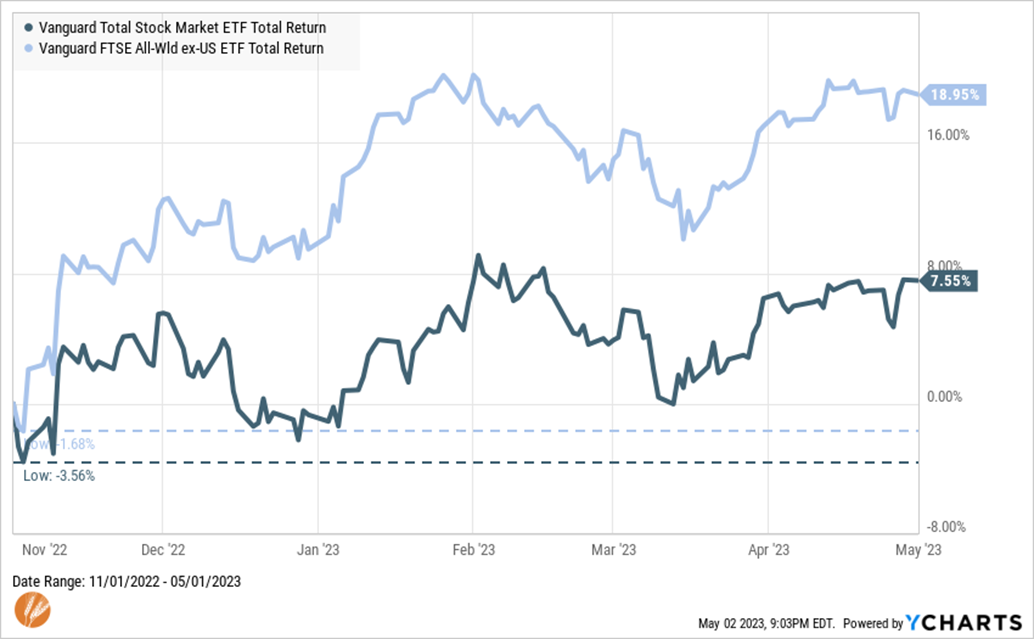

Investment firm Verdad Capital and Bloomberg data have done a similar analysis comparing valuations of US and International stocks. In October 2022, the gap between US and International valuation was at the 95th percentile of US being over-valued relative to International. Since then, International stocks have quietly outperformed US stocks but that gap remains at the 76th percentile - approximately double the long-term average difference.

Figure 6: During the mini-rally that stocks have had off of their October 2022 lows, international stocks have quietly led the way.

Emerging Markets’ valuation is also at a discount

Not to be left out, we can return to analysis from AQR regarding recent differentials between US stocks and those of Emerging Markets. They conclude that the valuation differential between Emerging Markets and Developed Markets (US and International Developed) is the widest it has been since 2002 and that Value stocks in Emerging Markets are at the 97th percentile for being undervalued relative to Emerging Markets Growth stocks.

History is a reference point, not a predictor

The above are all data points, not predictions, and are provided for historical context. And none of this is to suggest that the S&P 500 is on the cusp of another “lost decade” and Everything Else will outperform from this point. But over time, investment capital tends to flow to assets that are relatively undervalued compared to others. These tides can turn slowly and without warning. And they often happen when expectations for the recent market-leader are the highest and those of the recent market-laggards are lowest.

As we witnessed with SVB last month, it’s often the things that few expect which move markets. At that time, and after Credit Suisse’s demise, it was widely expected that Deutsche Bank would be the next casualty. Last week Deutsche Bank posted better than expected earnings, liquidity, and deposits. Sometimes things that everyone expects to happen don’t materialize. With expectations so high on the S&P 500, dominated by US Growth stocks, and expectations so low on Everything Else, the next 10 years of investment returns may look quite different from the last 10 years.

Perhaps Churchill’s quote about democracy being the worst form of government, except for all others that have been tried, can be applied to diversified investing. More narrowly focused investment strategies can be appealing when they are working but lack the robustness of diversification to sustain changing and unpredictable economic conditions and investor expectations. In an unknowable future, maintaining a diversified approach that has worked throughout multiple market cycles is the best way to approach investing for a long future.

Sources: Data from YCharts. Verdad Capital “Swedish Fish”, AQR “ReEmerging Equities” and “Value. Why now and Capturing the Comeback in its Early Innings”. Indexes: S&P 500, Russell 1000 Value, Russell 2000, Russell 2000 Value, MSCI All World ex-US, MSCI All World ex-US Value, MSCI All World ex-US Small Cap, MSCI All World ex-US Small Value, MSCI Emerging Markets. All Indexes represent total return including dividends. PVP Equity comprised of all component indexes and rebalanced annually.